Data and General Perspective

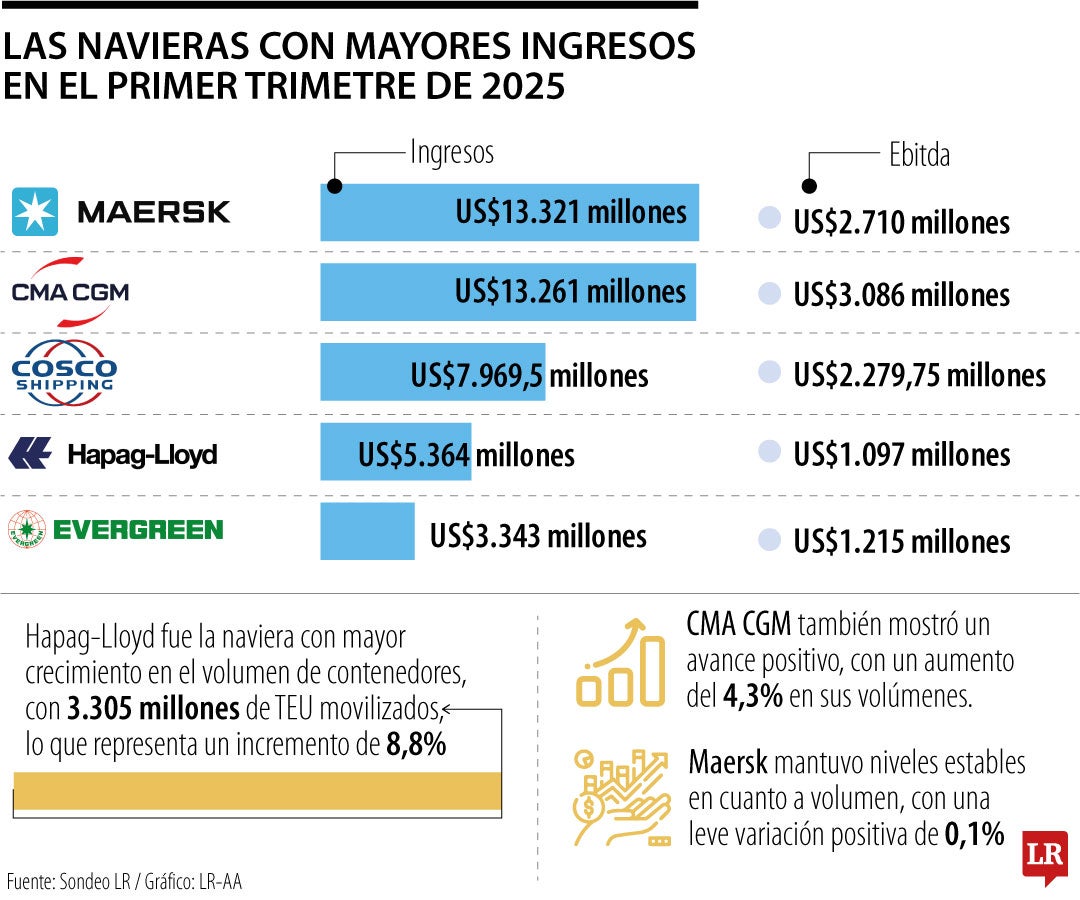

By the end of the first quarter of 2025, major shipping lines have reported robust revenues, alongside notable operational improvements that reflect the recovering global freight flows. According to data collected by Pórticolive and analyzed by La República, companies such as Maersk, CMA CGM, COSCO Shipping, and Hapag-Lloyd lead the revenue rankings.

Maersk holds the top position with revenues exceeding US$13.300 billion, marking an 8 % increase compared to the same period in 2024.

CMA CGM follows with approximately US$13.200 billion in revenues and an EBITDA above US$3.000 billion, driven by rate adjustments and route optimization.

COSCO Shipping recorded revenues of around US$7.969.5 billion, representing a 20 % year-on-year growth; the company also moved over 6 million TEU of containers.

Hapag-Lloyd, in fourth place, surpassed US$5.300 billion, with a growth of approximately 17 % versus Q1 2024, supported by a 9 % increase in volume across key maritime routes.

This ranking underscores a dual scenario: a firm market recovery in maritime shipping following global logistical disruptions; and the vital role of operational efficiency, rate adjustment, and capacity management in sustaining competitiveness. For shippers, exporters/importers—and especially logistics firms like CEA Cargo—these results signal clear opportunities and necessary areas for adaptation.

Implications and Opportunities for CEA Cargo

Emerging Challenges:

- Rate volatility demands cost‐coverage strategies and well-structured contracts to safeguard margins against unforeseen increases.

- Higher volumes put pressure on ports, terminals, and delivery times, necessitating optimized customs and logistics workflows.

- Competition among shipping lines for profitable routes may result in higher freight costs and variable lead times, affecting end-to-end supply chains.

Where CEA Cargo Can Add Value:

- Direct negotiation with shipping lines and strategic partnerships: Secure preferential rates, guaranteed space on vessels, and participation in more efficient rotations.

- Complementary logistics services: Offering full container loads (FCL) / less than container loads (LCL) consolidation, real‐time tracking, handling of special cargo, and door-to-door services to reduce lead times and minimize risks.

- Digitalization and traceability: Deploying tools that allow monitoring cargo transit, anticipating delays, and managing customs/regulatory documentation smoother.

- Sustainability and energy efficiency focus: Since operational costs such as fuel and regulatory compliance have a direct financial impact, there is room to differentiate by offering greener, more efficient solutions.